New drug inhibits cancer cell growth

A new compound starves the growth of cancer cells. Future anti-tumor drug for the future likely.

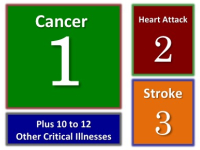

How do you decide when the insurance policy offers both a cancer-only as well as a critical illness insurance option?

How do you decide when the insurance policy offers both a cancer-only as well as a critical illness insurance option?

Here’s why you might choose the cancer-only option.

Firstly, in your 40s and 50s cancer is generally the bigger risk you face. A cancer diagnosis is more likely to occur than a heart attack or stroke. The same is true even in your early 60s.

Secondly cancer accounts for between 50% and 64% of all claims by those who purchased critical illness insurance policies. See the latest critical illness insurance claims information reported by the Association.

Thirdly, cancer insurance is far less costly. A good cancer-only policy is generally about one-third of the cost of a comprehensive ci insurance policy.

Finally, there’s a planning option never suggested to consumers. Buy a modest cancer-only policy in your 40s. That locks in your insurability. In your 50s, buy a critical illness insurance policy. Keep both or drop the cancer-only (once you have been health approved).

Costs for insurance policies can vary significantly. That’s why it always pays to compare. Click the FREE QUOTE button on the Advertisement to see quotes for BOTH cancer-only and critical illness insurance plans.

Unquestionably the advantage of a critical illness insurance policy is the fact that it will pay for many different illnesses. In addition to cancer, these policies generally pay benefits following a heart attack or stroke.

Unquestionably the advantage of a critical illness insurance policy is the fact that it will pay for many different illnesses. In addition to cancer, these policies generally pay benefits following a heart attack or stroke.

Here’s why you might chose the full or comprehensive critical illness insurance plan.

Firstly, heart attacks and strokes start to become a greater risk in your 60s. If you are in your 50s, having more comprehensive coverage makes sense.

Secondly you may be self-employed and have a high deductible health insurance plan. A modest, low-cost ci insurance plan can augment those uncovered health care expenses.

Finally, maybe you have been paying for life insurance and only now realize your risk of dying between now and age 70 is far less than your risk of an illness that can financially impact you and loved ones.

A new compound starves the growth of cancer cells. Future anti-tumor drug for the future likely.

Better cardiovascular health in midlife can reduce dementia risk later in life.

Adults with the healthiest sleep patterns had a 42 percent lower risk of heart failure.