New drug inhibits cancer cell growth

A new compound starves the growth of cancer cells. Future anti-tumor drug for the future likely.

Those who have more serious or frequent medical needs are at risk when they have a high deductible plan.

Those who have more serious or frequent medical needs are at risk when they have a high deductible plan.

Many of us are one diagnosis away from a most significant financial crisis. Consider that one American adult is diagnosed with cancer every 21 seconds and another has a heart attack every 40 seconds. Add to that accidents, pregnancies, diabetes and now, of course, the Covid virus.

You are likely to be impacted in three ways when you experience any serious health issue.

First, you are likely to reach your health plan deductible.

Second, you will likely face meeting out-of-pocket maximums.

Thirdly, you are likely to find not all health related costs (including the medications prescribed) are going to be covered by your insurance plan.

Finally, you’ll need time off for treatments and recovery. Time off equals less income to pay your rent, mortgage, child care, cell phone bills.

And, if all this wasn’t enough, here’s a face you don’t think about. You will still be paying your monthly health insurance premium whether you are working or in the hospital.

Following difficult financial times personal bankruptcies skyrocket.

Following difficult financial times personal bankruptcies skyrocket.

In 2006, 597,965 Americans filed for personal bankruptcy.

By 2010, the number soared to over 1.5 million.

A Harvard University study found that two thirds of bankruptcies were linked to medical and health-related bills.

Most of those filing for bankruptcy were middle class and had health insurance.

Hospital bills were the largest single expense for about half of all medically bankrupt families; prescription drugs were the largest expense for 18.6 percent.

We believe some coverage is always better than no coverage. In your 40s and 50s the Association suggests pricing both a cancer-only as well as a full ci insurance policy. The better companies today offer you both options within one policy.

Our suggested formula is coverage equal to between six (6) and 18 months of your rent or mortgage payments. That should be more than enough to cover your bills.

And, if any money is left over, you can use it to take that well deserved trip or family vacation.

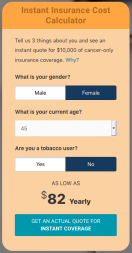

SEE WHAT $10,000 of cancer insurance might cost. Use the Association’s Cost Calculator.

SEE WHAT $10,000 of cancer insurance might cost. Use the Association’s Cost Calculator.

If your company offers employer critical illness insurance, read our suggestions for comparing coverage and getting the best value and options.

Finally we post ways consumers can compare critical illness insurance policies to find the best rates and options.

A new compound starves the growth of cancer cells. Future anti-tumor drug for the future likely.

Better cardiovascular health in midlife can reduce dementia risk later in life.

Adults with the healthiest sleep patterns had a 42 percent lower risk of heart failure.