A cancer-only policy can be a highly affordable choice. Many people are far more worried about being diagnosed with cancer sometime before they turn 65 or 70. It’s true that there is a real risk.

A male age 40 who is a non-smoker could pay as little at $67 a year for $25,000 of cancer-only insurance. If he is a tobacco user, he’ll pay around $95 a year. That’s about $8 a month.

A male age 40 who is a non-smoker could pay as little at $67 a year for $25,000 of cancer-only insurance. If he is a tobacco user, he’ll pay around $95 a year. That’s about $8 a month.

The chances of getting cancer at age 40 are low. It does happen but we acknowledge that it is low.

The chances of getting cancer in your 60s is much higher.

Our male who is 40 today, will pay about $5,600 in total between now and when he is age 62.

If he is diagnosed with cancer at age 62, the good news is that he will very likely not die. But he will need to take months off for treatment and to recover.

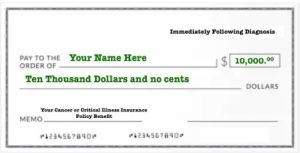

That $25,000 payment from his cancer insurance will sure come in handy. Because he knows his mortgage or rent is covered, he can focus on what is important – recovering.

Is that cancer insurance policy worth it? To him it will be worth every dollar in premium spent. To his family as well.

When you reach age 50, you probably start to think about health risks like heart attack and stroke. They are more likely to happen at older ages.

A $10,000 comprehensive critical illness insurance policy will cost around $252 a year for a male age 52. That is about $21-per-month. This is the non-tobacco user rate. If he smokes, the cost will be almost twice. His risk of disease as a smoker is also significantly higher.

A $10,000 comprehensive critical illness insurance policy will cost around $252 a year for a male age 52. That is about $21-per-month. This is the non-tobacco user rate. If he smokes, the cost will be almost twice. His risk of disease as a smoker is also significantly higher.

Women may pay less than men. The $10,000 benefit will cost a woman age 52 around $199 a year. If she smokes, she will pay around $308 a year.

Since you have read this far, we want to say thank you. Specifically we hope you better understand why we believe this important protection can be worth it.

Since you have read this far, we want to say thank you. Specifically we hope you better understand why we believe this important protection can be worth it.

Because the risk of cancer is real.

Undeniably no one wants to get ill.

Unquestionably critical illnesses happen.

Obviously they happen to good people like you and me.

Rather than just avoid the issue, take some action.

Indeed even a small policy can be better than no plan at all.

New drug inhibits cancer cell growth

A new compound starves the growth of cancer cells. Future anti-tumor drug for the future likely.

Better heart health in midlife lowers late-life dementia risk

Better cardiovascular health in midlife can reduce dementia risk later in life.

Insomnia heart disease; 42% reduction in heart failure

Adults with the healthiest sleep patterns had a 42 percent lower risk of heart failure.